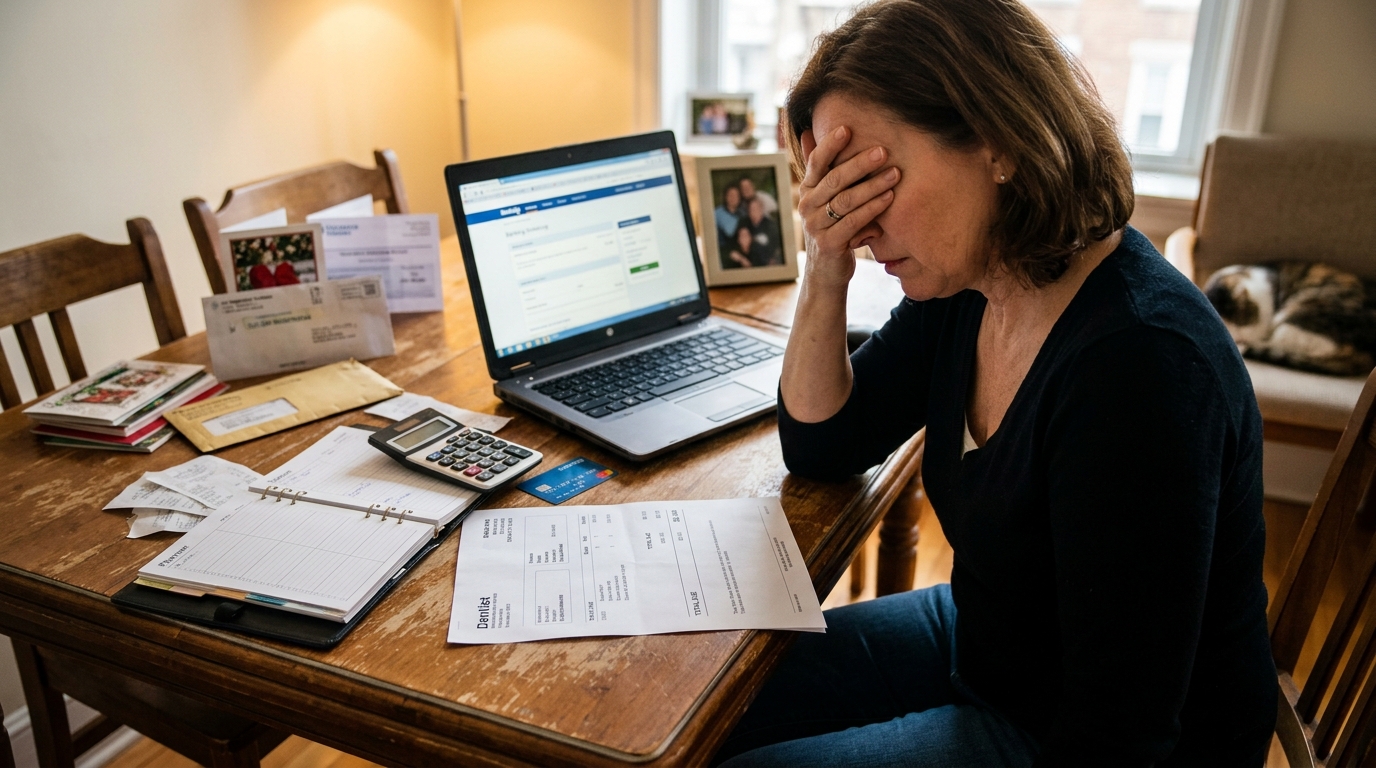

The bill that broke me came from the dentist. Two root canals, a crown, and the phrase “your insurance doesn’t cover this” delivered with the calm of someone who’d said it many times before. The total was $2,400, and I sat in my car afterward staring at my phone, doing the math on how many paychecks that represented, and realizing — with genuine panic — that I had nowhere to take the hit from. My emergency fund was for emergencies. My checking account was already committed. The credit card was doable but painful.

What I didn’t know that afternoon was that the system that would eventually end this kind of panic for me had a name, had been around forever, and was almost embarrassingly simple. Sinking funds. A bucket system where you save for predictable-but-irregular expenses before they happen instead of improvising through them after.

It took me a full year of running sinking funds before the underlying anxiety about money actually quieted. I want to walk you through how I set them up, which categories turned out to matter most, and the one kind of expense I still get wrong. If you’re sick of being ambushed by bills that shouldn’t, technically, be surprises, this is the system that finally did it for me.

The $2,400 Dentist Bill That Broke Me

I had what I would have called, at the time, a solid financial situation. I had a $5,000 emergency fund. I wasn’t in credit card debt. I was putting money into retirement. My budget, as I understood it, balanced every month.

What I didn’t have was any framework for expenses that were bigger than my monthly budget but not technically emergencies. Car registration. Annual insurance premiums. Christmas. Vet visits. The dentist. Plane tickets to visit family. My laptop dying after five years. None of these are emergencies — they’re predictable life. But because they didn’t land in my monthly budget, every one of them felt like a crisis when it arrived.

The dentist bill was the one that made it obvious. Driving home, I realized I’d been running my finances on a pattern of budget-for-the-month, panic-when-something-bigger-happens, slowly-recover-over-the-next-quarter. Every year had a dentist or a car or a furnace. Every year I was surprised by it. That can’t be an emergency fund situation if it’s happening three times a year, every year.

I started researching how other people handled this. The system that kept coming up in personal finance circles wasn’t sophisticated. It was a simple idea: if you know an expense is coming, divide it by the number of months until it hits, and save that amount every month into a dedicated pot. When the expense hits, you already have the money. No emergency. No credit card. No surprise.

What Sinking Funds Actually Are (And Aren’t)

The term is borrowed from corporate finance, where it means a fund that’s being set aside (or “sunk”) for a future known obligation. In household finance, it’s the same idea: money you save forward for things you know are coming.

A classic personal finance book pointed me toward the concept, but the specific household implementation I built is simpler than what any one book prescribes. It’s essentially this:

- Each category has its own “sinking fund” — a tracked balance.

- Each month, a fixed amount moves into each fund.

- When an expense in that category happens, you pay from that fund.

- Funds don’t reset at the end of the month. They accumulate until used.

What they are not: an emergency fund. The emergency fund is for genuine surprises — job loss, catastrophic medical, the kind of thing you truly can’t plan for. Sinking funds are for things you can plan for but don’t happen every month. The two serve different purposes and I keep them as separate pots.

They are also not budget categories in the normal sense. A monthly grocery budget resets each month. A sinking fund accumulates. This distinction matters because sinking funds, by design, look like “unspent money” in your checking account. If you don’t track them separately, you’ll spend them on something else and then be blindsided when the expense shows up.

The mental shift that made the system click: predictable doesn’t mean monthly. A car registration is predictable. Property tax is predictable. Your kids’ birthdays are predictable. The dentist every six months is predictable. Treating these as if they are surprise expenses is a failure of imagination, not a failure of income.

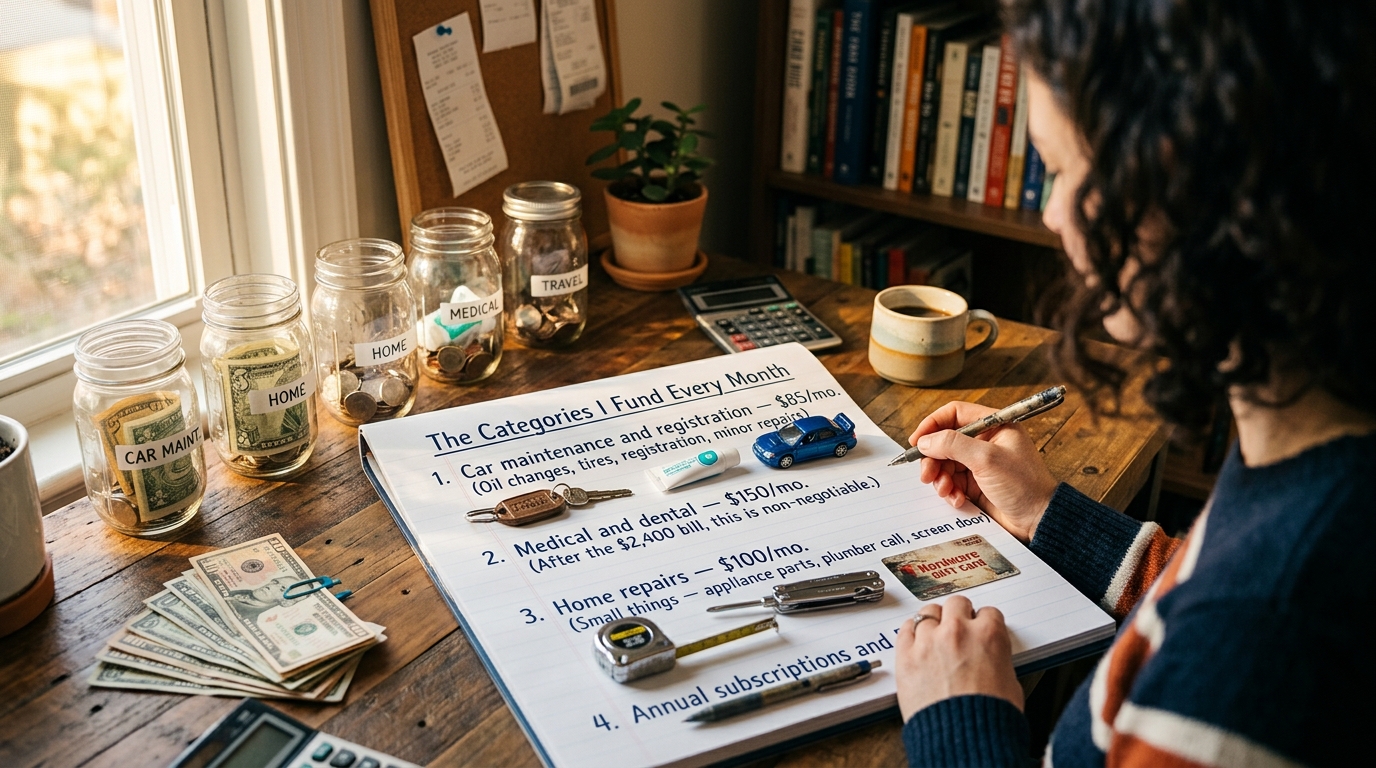

The Categories I Fund Every Month

Here is my actual list of sinking funds, in rough priority order, with what I allocate to each month. Your numbers will differ, but the categories are the shape of it:

- Car maintenance and registration — $85/mo. Covers oil changes, tires, registration, minor repairs.

- Medical and dental — $150/mo. After the $2,400 bill, this is non-negotiable.

- Home repairs — $100/mo. For the small things that come up — a broken appliance part, a plumber call, a damaged screen door.

- Annual subscriptions and insurance — $65/mo. Domain renewals, annual memberships, any insurance paid annually.

- Holidays and gifts — $75/mo. Birthdays, Christmas, Mother’s Day, anniversaries. All of it.

- Travel — $125/mo. The only one I look at as “fun.” Plane tickets, lodging, the trip itself.

- Pet care — $30/mo. Vet visits, not routine food.

- Electronics replacement — $40/mo. My laptop, my partner’s laptop, the phones, the router — all of these will die on their own timeline.

- Car replacement — $150/mo. Long horizon, but I want the next car to be a cash purchase.

- Kids’ school costs — $50/mo. Fees, supplies, field trips, the one summer camp.

That’s $870 a month across ten funds. That’s real money, and setting it aside required some meaningful tightening when I started. But the first time something went wrong and I just… paid for it out of the right fund, without flinching, I understood why the system is worth it.

I keep an old-school budget planner notebook where I write the balances at the start of each month. It’s analog, it’s slow, it’s silly, and it’s why I actually see the numbers. Apps let me tune them out.

How I Set Up the System (Online + Offline Hybrid)

I went through three versions before landing on one that worked. The final setup is deliberately simple.

One checking account for spending. Bills and groceries run through here. Normal budgeting behavior. I treat this as the working account and try to keep it lean.

One high-yield savings account for sinking funds. This is where all the sinking fund money lives in a single balance, earning interest. The “funds” themselves are tracked in a spreadsheet, not in separate bank accounts. Multiple accounts is more work than it’s worth.

A spreadsheet that tracks each fund. Ten rows, three columns: category, current balance, monthly contribution. At the start of each month I add the contributions. When I spend, I subtract. The savings account total should always equal the sum of fund balances, minus whatever sits in my emergency fund (which is in the same account).

An automated monthly transfer. On the first of every month, my checking account transfers $870 to the savings account. I never have to decide to do it. The decisions happen in the spreadsheet, not in the transferring.

I print the spreadsheet monthly and keep a copy clipped to the fridge. This feels ridiculous to some people. For me, seeing the numbers in physical form is what keeps them real. I’ve tried purely digital setups; I’d stop looking at them after a few weeks.

The tool that finally made spreadsheets viable for me was a printing calculator for doing the end-of-month totals. Silly, I know. But the friction of tallying numbers on a phone was just enough to make me skip it. The calculator, sitting next to my budget planner, makes it a five-minute ritual.

The Stress That Disappeared (And What I Didn’t Expect)

A year into running sinking funds, the dominant change isn’t financial. It’s emotional. Things that used to trigger genuine panic — a dental appointment, a check-engine light, a Christmas season approaching — just… don’t anymore.

The emotional shift broke down into three parts I didn’t expect.

First, decision fatigue dropped dramatically. I used to waffle on every non-essential spend because I didn’t know if I could afford it. “Can we do the weekend trip?” required mental math through three buckets of uncertainty. Now I look at the travel fund and know exactly how much I have to spend. The answer is either yes or no; there’s no more gray zone.

Second, fights about money lessened. My partner and I have always had different money styles. The sinking fund system gave us a shared language. We stopped arguing about whether a purchase was a good idea and started asking which fund it came from. If the fund had money, the purchase was fine. If the fund didn’t, we didn’t do it. End of argument.

Third — and this is the one I didn’t see coming — I became more generous. When I wasn’t walking around with low-grade financial anxiety, I found I was more willing to pick up the tab, donate to things I cared about, and say yes to friends when they asked for help. Anxiety makes people tight. Security makes people generous. I’d always assumed the relationship went the other direction, but I think I had it backwards.

A year in, I now have a year of data. The car maintenance fund overshot (we didn’t have a big repair). The medical fund was exactly right (two minor procedures I paid for without blinking). The travel fund was spent to zero (worth every penny). I adjusted the contributions going into year two based on what I learned.

Final Thoughts: Small Pots, Big Peace

The thing I wish someone had told me twenty years ago: most financial stress isn’t about income. It’s about unpredictability. I’ve had years where I earned more than I do now and felt broke. I’ve had years where I earned less and felt secure. The difference was almost always whether I was being repeatedly ambushed by expenses I should have seen coming.

Sinking funds are just a mechanism for converting unpredictable expenses into predictable ones. That’s all. But that one reframe, when you actually commit to it, changes the texture of your financial life in ways that are hard to overstate until you’re on the other side of it.

I also want to be honest about one thing I still get wrong. The category I underfund consistently is home repairs. Old houses don’t care about your spreadsheet. I’ve been hit twice in the last year with home issues bigger than my home repair fund, and both times I had to borrow from another fund to cover it. I’m still adjusting my contribution upward. Every year you run this system, the numbers get closer to reality. They don’t start accurate.

Save for what you know is coming. That’s it. That’s the whole strategy. Everything else is detail.

If you’re going to try this, start with three funds, not ten. Pick the three categories that have hurt you most in the last year. Open a savings account. Automate a transfer. Track the balances in the dumbest, simplest way you will actually look at. Adjust the numbers after three months based on what you see.

The first time something breaks and you pay for it without a twinge, you’ll understand why this system — which sounds like accounting homework — is actually one of the more meaningful pieces of peace you can build into your life.

Leave a Reply